December 21, 2007 was the day Lesia and I submitted our final payment to eliminate $150,000 in debt. One of the unique things I have learned is that it is possible to become comfortable living debt-free just as easily as it is living in debt. However, the former involves a much lower level of stress.

Before we were married, conversations about money were common. After we were married, that practice continued with an added level of intensity. One of the main reasons we decided to eliminate debt was so we could buy our lives back. We had reached a point where we realized that every company to which we owed money owned a little piece of us.

No matter where you are in your financial journey, progress is always within reach. Each successive financial decision you make has one of two consequences; wealth is either moving toward or away from you. The main factors that influence your outcomes are discipline and behavior. For example, discipline will allow you to save $200 every paycheck, but behavior will make you leave it alone.

As I think about the past 14 years, one of the lessons I have learned is that money can only follow the instructions you give it. Just about every financial outcome begins with a decision, either made by you or someone who has influence on your life. If you are not satisfied with your current relationship with money, that can change depending on what you decide to do with the next dollar you earn.

If you would like to learn more about our journey to debt-free living, check out the NerdWallet and Black Enterprise articles featured on our In The News tab: https://www.gametimebudgeting.com/new-page-3. If you prefer a more in-depth version, my book - The Uncommon Millionaire – is a great resource. Here's a link: https://amzn.to/3AYlEtQ

How Happy Are You?

Most people, in general, want to live long and live well. Longevity probably has more to do with what is at the end of your fork or spoon. Mix in a little daily exercise and you may discover your personal fountain of youth. On the other hand, living well is a phrase many people use, but its actual definition often depends on the person. For example, what does living well mean to you? Ask a family member or your best friend the same question and their answer may differ greatly.

The World Happiness Report 2021 ranks Finland as the happiest country in the world. It highlights six significant factors which contribute to happiness: gross domestic product (GDP) per capita, social support, life expectancy, freedom to make life choices, generosity, and corruption levels. Gross domestic product is the total value of goods produced and services provided in a country during one year. Although the United States has the highest GDP in the world at approximately $20 trillion, it ranks 19 on the survey of happiest countries.

On an individual basis, earning above $60,000 to $75,000 per year in income would not achieve a higher level of emotional well-being according to a Purdue University study. To put it another way, millionaires and billionaires may not be happier than you are at this moment. They have more money and wealth, so people assume they have a happier life. Not true!

If you’d like to improve your personal happiness score, implement the following tips:

Spend more time with people you love and who love you in return - In today’s high-tech world, this can be done virtually with ease; however, there’s much to be said for personal human-to-human interaction.

Allow time for yourself – If you like to read, write poetry, watch movies, hike, go to the gym, or volunteer, do more of it.

Be kind to others – The world would be a very different place if people treated others the way they wanted to be treated.

Gain some form of independence – Your first true taste of being independent usually happens when you start living on your own without any assistance from your parents. If you require minimal supervision on your job because you are a master at your craft, that’s another form of independence. Managing your money in a way that allows you to save, invest, spend, and give can also lead to financial independence.

Your desired level of happiness is up to you. Because you can’t go to a store and purchase happiness by the pound, it’s something you have to strive to achieve on a daily basis. Nobody can do it for you.

May the rest of your life be the happiest ever!

Three Financial Fitness Principles You Should Follow

How Much Is Enough?

Most Americans are engaged in an endless pursuit of more on a daily basis. More comes in many different forms: intangible things like love and approval or things you can see and touch like homes, cars, clothes, and money. If none of these wets your appetite, more for you might be the current items in your Amazon shopping cart. The peculiar thing about more is that after whatever you desired is in your possession, the thrill associated with it quickly fades. As a result, the pursuit of more starts again.

Instead of searching for more most of your life, try chasing something that may bring an added bonus—contentment. When you find that state of peaceful happiness, your world will slowly begin to make sense. You will learn that some of the things you thought were important don’t matter as much. You may discover that what you thought you once desired was actually based on the outside influence of family, friends, or repetitive marketing messages designed to stimulate your emotions.

As an example, when people acquire more money, one of the normal patterns of behavior is to spend more. Money was never the real goal. It is only the medium by which something else could be secured to produce a specific feeling. If you take money out of the equation and ask the average person why they do anything, one response that is lurking just beneath the surface of complete honestly is… because I felt like it.

Satisfying those feelings comes at a cost. In the financial world, the dollar you spend today could be costing you four dollars of financial security, peace, and comfort in the future. Regarding money and your pursuit of more, have you ever asked yourself, “What is preventing me from saving/investing a larger amount on a monthly basis to better prepare for the higher cost of the life I want in the future?”

How much is enough? Only you can answer that question.

Tips to Develop a Millionaire Mindset

Ready For Your Final Boarding Call?

Last week, Al received a large manila envelope in the mail from his mom. He opened it, took a quick glance, and placed the contents on the dining room table. Because he got distracted, it remained there. A few minutes later, his wife said, “What’s this?” She picked it up and remarked, “Oh my God! That’s spooky.” Al’s mom had mailed an updated copy of his dad’s obituary. To Al, it was just a document to be filed. To his wife, it represented something much more emotional. Hopefully, his parents will be around for many more years, however, everyone must embrace the fact that nobody lives forever.

Most people find discussing death about as interesting as talking about a colonoscopy. At least with the latter, you should wake up when it is over. However, everyone has that final appointment that cannot be canceled or rescheduled. Just because you may not like discussing your expiration date does not mean you should avoid planning for it. During a recent conversation Al had with one of his financially savvy friends, Derek stated, “I have a will and life insurance because I care about the people I love.” Basically, if you are married, have kids, or a positive net worth, documenting your end-of-life plan is important and taking the necessary steps to prepare financially is crucial.

According to the GoFundMe website, they perform over 125,000 memorial fundraisers each year and raise over $330 million+ per year. There is nothing wrong with people donating to the cause of their choice. However, when you plan in advance, that forethought can often reduce the financial burden on others. This is particularly important for people who have children under the age of 18. If something happened to you unexpectedly, do you have enough life insurance to ensure your dependents are provided for and your celebration-of-life service is covered? If not, direct cremation might be a viable, less costly option. At least this inexpensive one-way ticket will hopefully leave more insurance money to take care of your heirs.

The time spent preparing this information should be one of the top items on your Adulting list. If you know something is going to happen in the future, it is wise to plan for it. When Al and Lesia got married, one of the to-do items on their list was preparing a last will and testament. A few years later, they transitioned to the Lesia and Alfred D. Riddick Family Revocable Living Trust. One of the best advantages of having this document in place is peace of mind which is priceless.

The following items should be considered when planning for your final boarding call:

· Visit Policygenius.com to compare life insurance quotes from various companies

· Prepare a living will and healthcare power of attorney (see OH example)

· Determine your needs - Will vs Trust

· Establish Payable on Death bank accounts

· Secure and protect your digital legacy

Safe travels! 😊

What If $1 Million Is Not Enough!

According to The Global Wealth Report (2021), there are approximately 21 million millionaires in the United States. If you are a member of this group, congratulations! If not, practicing strategic saving and investing behaviors might help you get there by the time you retire.

One of the questions that is easy to forget when planning for retirement is, what does it cost to be you? Having an estimate of your monthly bills in your mind is different than doing the math based on facts. When you are not in the habit of tracking expenses, it is easy to forget spending on gifts, vacations, travel, and home décor while planning for retirement.

Several areas should be taken into consideration before the transition from paid to unpaid work:

· Lifespan – The longer you live, the more money you will need. Depending on your family history and current health status, it is possible that you might make it to 80 years old or beyond. National Center for Health Statistics

· Geography – Where you live has a major influence on how long your retirement nest egg will last. A million dollars in New York City or Los Angeles will not go as far as it will in Huntsville, AL. Cheap Places to Live

· Retirement Income – Social Security might not be able to buy the life you hope to have in retirement. However, whatever amount you receive could slow how quickly funds are depleted from your retirement accounts. Retirement Income Calculator

· Health – Health costs tend to rise as you age. Much of how you live your life in your 40s and 50s, in addition to genetics, will impact your quality of retired life. Consistent exercise and healthy eating actually increase total health care costs due to a longer lifespan. That’s a good thing! Health Care Costs in Retirement

· Lifestyle – If being a free-spirited spender during your working years is a habit, that behavior is even more unsustainable during retirement. Most people do not realize their income drops dramatically when supporting themselves from savings accumulated during their working years.

· Inflation - One million dollars usually has less buying power in the future, in contrast to today, due to a gradual increase in prices which decreases the purchasing value of money.

There is not a one size fits all for retirement planning. Hopefully, focusing on these six categories should prepare you for the life you want as you ride off into the sunset. One million could be enough for some, but not for others. The choice is yours!

10 Money Saving Travel Tips

Domestic travelers in the United States spent $927 billion in 2019. After the sharp decline in 2020, more people are now being vaccinated. The constant increase in travel bookings signal a return to a more normal way of life. Although the monthly personal savings rate has been in the double digits for the past year, remember to implement the following tips so you don’t break the bank during your next trip:

· Redeem sky mile rewards – Frequent travelers often prefer to earn airline miles for day-to-day credit card purchases. Your sky miles account balance might yield a round trip ticket to your next destination.

· All weekdays aren’t created equal – The best days to fly for cost conscious travelers are Tuesdays or Wednesdays depending on the route. The second best are Mondays, Thursdays, and Saturdays. The most expensive days to fly are Fridays and Sundays.

· Early birds and night owls fair best – Early morning and late evening flights are usually less expensive. Be prepared to give up your seat on an overbooked flight for a voucher (if you have the time).

· Book your car before booking your flight - Hertz Global Holdings, Avis Budget Group and Enterprise Holdings sold off inventory during the pandemic. There are more customers than cars and prices have increased.

· Utilize hotel ground transportation – Many hotels offer guests free ground transportation to and from the nearest airport. Pick up your rental car from an off-airport location near your hotel and save approximately 15% in taxes and fees.

· Beware of the hotel mini bar – Weary travelers can be tempted by the readily available chocolate bars, cookies, potato chips, wine, soda, and bottled water. These items are usually marked up 3-4 times the usual price.

· Pack your lunch – When traveling by plane or car, utilizing a brown bag usually creates healthier meals in addition to saving money.

· Before you go, count the cost – Your travel budget may include a combination of the following expenses: airfare, airport parking, rental car (gas), lodging, tolls, food, shopping, and tips (maid service, baggage attendants, bartenders).

· Consider travel insurance – Your decision should take into account whether or not your trip is refundable, the amount of coverage you might already get from your credit card, and where you’re going. Remember! United States-based health insurance policies generally offer coverage only within the U.S.

· Upon return, start saving again – Establish a travel savings account which should also appear as a monthly budget line item to protect against going into debt for your next adventure.

Your adherence to social distancing, hand-washing, and mask wearing has created an opportunity to travel like the good ole’ days. If you’re going to spend money, you might as well get the best bang for your buck.

Money Earned from Working Can Suck

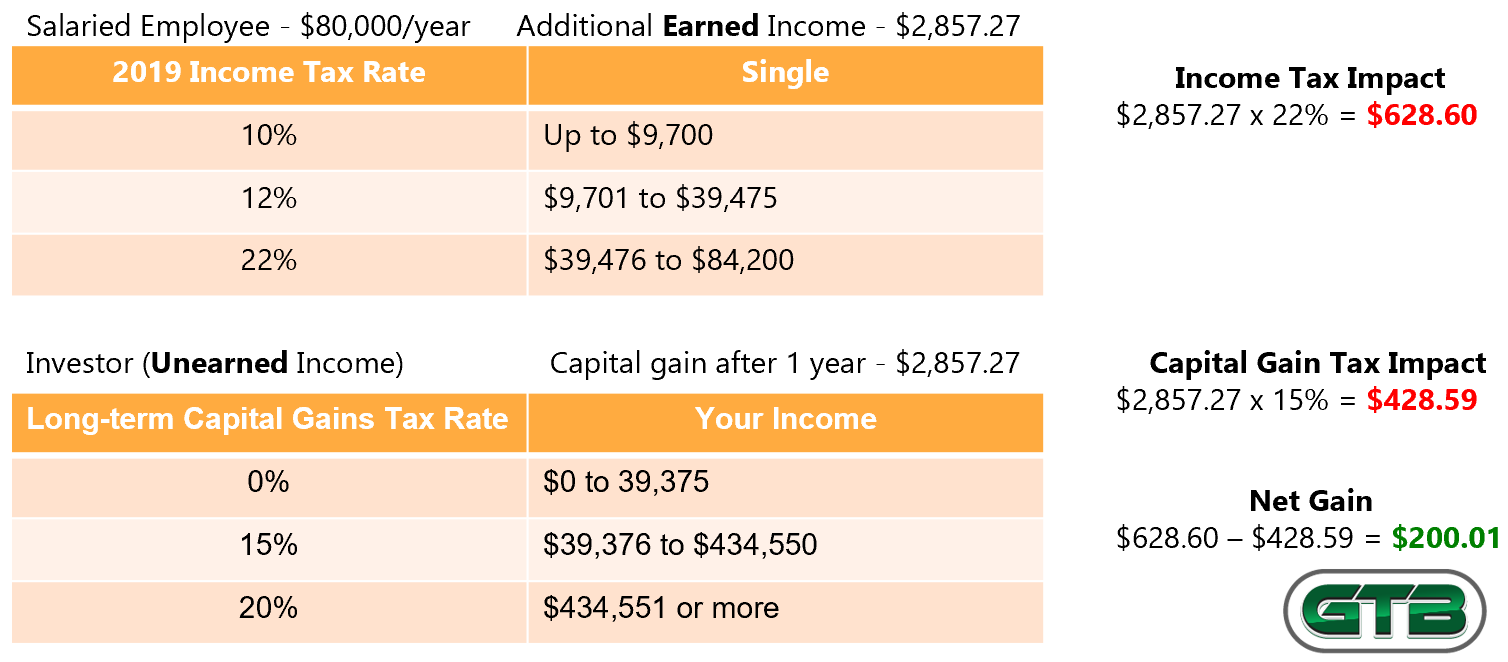

One of the secrets to getting and staying rich comes down to how your money is earned. Money earned from investing is taxed at a lower rate than money earned from working. The terms unearned income (e.g., from investments) and earned income (e.g., from a job) can have a profound impact on your ability to build wealth.

The following picture shows the cost basis summary for an investment account. Cost basis, in a broad sense, refers to the price you pay for shares of an investment. When you invest, two of the potential rewards are dividends and capital gains. A dividend is a sum of money paid, usually quarterly, by a company to its shareholders out of its profits. Various mutual funds and exchange-traded funds (ETF) also pay dividends. A capital gain refers to an increase in the value of an asset. It is realized when that particular asset is sold. A capital gain can also be unrealized which means that the increased value of an investment is only on paper. For example, if you paid $1,000 for 10 shares of a $100 stock and then the stock price went to $105, your $50 capital gain would only be realized if you sold the stock. If you didn’t sell, the capital gain would be unrealized. As additional information, a capital loss would be realized when selling an asset for less than what you paid for it.

Assume the above information belongs to a fictitious character by the name of Stacy. She’s single and earns $80,000/year. She decides to sell all the shares of this ETF held for more than one year. In the above picture, note the capital gain/loss column heading and the $2,857.27 listed under long-term. Short-term capital gain/loss represents shares owned for less than one year. When Stacy sells this asset, she will need to pay taxes.

Based on your knowledge about taxes, what tax rate do you think will be applied to this capital gain? A) 0% B) 15% C) 20% D) 22%

The following image shows how Stacey’s $80,000/year income puts her in the 22% tax bracket. If she had worked more hours on her job to earn $2,857.27, she would owe $628.60 in taxes. However, because she sold shares within her investment account, the capital gains tax rate of 15% (answer B) applies based on her income. She would owe only $428.59 ($2,857.27 x 15%) in taxes. The difference in taxes between Stacy working for money and money working for her is $200.01 ($628.60 - $428.59). All income from work is honorable; however, money earned from a job is more expensive. The tax treatment of unearned income provides a better understanding of why rich people choose not to work for money and let money work for them.

A Polo Shirt and Lobster Roll Teach Financial Lessons

One of Al Riddick’s favorite pastimes is eating seafood (actually any good food). His wife, Lesia, recently discovered his favorite food truck, The Wicked Lobstah, was returning to Dayton, OH. A few weeks ago, Al started making his own lobster rolls but thought this would be a neat day trip since the weather forecast was sunshine and 60 degrees.

Before leaving home, Lesia grabbed a shirt she had ordered from Nordstrom Rack and mentioned that they could stop by their Beavercreek location. Upon walking inside the store, Lesia said, “It shouldn’t take me long. I’m just making a return.” Based on past experience, Al knew they would be inside Nordstrom Rack for at least 30 minutes, so he went to the men’s section.

The first thing that caught his eye was a beautiful, big, red sign that read CLEARANCE! To Al’s surprise, he found a HUGO BOSS polo shirt, but after noticing the $59 sale price, he put it back. Al then noticed another HUGO BOSS shirt that was on sale for $11.99 (original price - $88). He asked the sales clerk if the $59 price was accurate since the only difference was that the $11.99 shirt had one line of a different color going down the front.

Al then started thinking about how some people, who have consumer debt, get further into debt simply because of practicing destructive behaviors. For example, let’s say Al decided to get the $59 shirt, but didn’t have the money in his checking account. Like many people, he may have thought, “I’ll put it on my credit card and then pay it off when the bill comes.” When you want something bad enough, you’ll make any excuse to get it. That’s the secret to why revolving (e.g., credit cards) and installment credit is so profitable. This is the question Al should have asked: What financial behaviors do I exhibit that are preventing me from having $59 to buy this shirt?

Al also thought about how easy it was for him to justify spending $17 on a lobster roll in contrast to how he chose not to spend $59 for a polo shirt that had a lower cost per use value. In Al’s mind, eating good food is a dining experience while buying clothes, on the other hand, doesn’t make him feel warm and fuzzy on the inside. Again, this is just another emotionally charged rationalization. The example presented was very basic; however, the same emotional response applies to financing homes, cars, and vacations.

If you’re wondering, Al decided to purchase the $11.99 HUGO BOSS shirt after the sales clerk scanned the tag and discovered it should have been priced at $59. She told Al he could buy it for the price as listed. As you may have guessed, he couldn’t resist an 88% discount.

Al Played the Lottery and Won

The lottery is based on luck, but if you have the winning ticket, you’re luckiest of them all. Recently, Al was feeling adventurous so he played the Powerball and paid an extra $1 for the Power Play, a multiplier that increases the payout. To his surprise, he discovered that his ticket matched the Powerball number. His $3 investment produced $12 (300% return). When he went to pick up his winnings, the cashier was shocked to learn he didn’t want more lottery tickets. As you may have guessed, he couldn’t comprehend playing again when he was already a winner.

This month is almost over, but remember that your monthly budget is more predictable than the lottery. Instead of spending money and hoping for success, you can create success by telling your money how to behave. All it takes is a simple and easy to duplicate plan that relies more on math than emotion. Your winning numbers can be found in the financial system you follow after receiving each paycheck.

9 Financial Tips for the New Year

10, 9, 8, 7, 6, 5, 4, 3, 2, 1! Happy New Year! These are the words millions of people will say once the clock strikes midnight on December 31, 2020. Within a few days of celebrating the beginning of 2021, you might make a New Year’s financial resolution. Unfortunately, over 80% of people who make them will have failed by the second week of February. Don’t worry! This statistic will not apply to you unless you decide it will.

If you would like to achieve a New Year’s financial resolution, follow these tips to increase your chance of success:

Be committed; don’t just try. The word try implies that failure is an option. Once you commit to do something, you will find a way to get it done if your why is big enough.

Analyze financial lessons from 2020. This past year has been unlike any other you’ve experienced in your lifetime. Hopefully, you’ve identified opportunities to improve your financial game plan for next year. If you repeat the same behaviors, you’ll get the same results.

Adjust your behaviors. Write a list of potential outcomes if you decided to modify at least one behavior that could positively impact your financial future. Regarding your financial success, behavior plays just as big a role as intelligence, sometimes more.

Establish a savings goal for 2021. Mastering the art of saving usually prevents you from overspending. Setting a savings goal and creating a plan to hit the goal produces small wins that add up over time.

Measure the gap between income and spending. As you prepare your January 2021 spending plan, determine the difference between income and spending for December. If you repeat this process each month, you will either be satisfied or unsatisfied with your financial progress for 2021. The choice is yours.

Pay yourself in installments. Project what major expenses will incur during 2021 and start saving immediately. If you know you have a $600 bill due on April 1, it’s much easier to save $200 every month during January, February, and March. This small, but significant tip can help you better manage cash flow and reduce financial stress.

Create and follow a monthly spending plan. You have a system for just about everything in your life; money should follow a system as well. While preparing your financial plan for January, develop a budget that is simple and easy to duplicate (teach me how to budget like a pro). Capture every expense and remember to give every dollar an assignment. Don’t forget about your monthly installment payments for that future big expense. Repeat this process every month.

Retrieve a copy of your credit report. Develop a habit of checking your credit report at least once every four months. Currently, each of the three major credit reporting bureaus are offering free weekly online reports through April 2021. Please visit www.annualcreditreport.com.

Measure investment performance. If you have pre- or after-tax investments, determine what you contributed during 2020 and assess the growth or decline in your account’s value. Depending on your goals, you might need to invest more or adjust your asset allocation.

After the clock strikes midnight on December 31, you have 365 days to make your financial dreams come true. Breaking down your yearly goals into monthly milestones almost guarantees success. On your mark, get set, go!

Let's Get Financially Naked

When someone at your doctor’s office says, “Will you please take off your clothes?” you probably aren’t offended. However, there are certain financial questions many people consider to be forbidden because the answer would make them feel naked: How much money do you earn? How many credit cards do you have? What is the balance in your checking account? Revealing answers to these questions are insignificant because they do not provide any insight regarding your ability to manage money.

While recording a guest segment for a radio show the other day, Al stated, “My wife and I live a very simple life. We have only 23 line items in our monthly budget.” After the interview concluded, the host, expressing disbelief in that low number of categories, mentioned he wanted to discuss these items on the next show.

If you doubt that it is possible to maintain a household utilizing 23 expense categories, here’s a summary of Al & Lesia’s monthly budget line items:

As you can see, this list is very basic. Items with an asterisk represent future high dollar expenses that are paid in a lump sum. For example, if you have several insurance policies with the same company, pay your premiums in full to take advantage of a larger discount (#MoneySavingTip).

There are a few items that are not on their list: mortgage, student loans, credit cards, and car payments. If you’re thinking about yourself, financially naked at the moment, and considering a weight loss, start with paying down your credit card balance. The lower the number of expense items in your monthly spending plan, the better. A revolving balance is like still having love handles after sticking to a meal plan and exercise routine for months without seeing any positive results.

If you haven’t been financially naked in a while, it’s time to bare it all in hopes of uncovering new opportunities to have more, spend wisely, and live abundantly. If you don’t like some of the love handles you discover while exploring your financial nakedness, a slight change in behavior can usually fix it.

6 Advantages of a Health Savings Account

The latter part of October is usually the time of year when employers kick off their annual open enrollment. During this two- or three-week timespan, employees have the opportunity to sign up for various healthcare options, insurances, a flexible spending account (FSA) or health savings account (HSA). To take advantage of the HSA, you must be enrolled in a high deductible health plan (HDHP). There are many benefits of utilizing a health savings account:

Triple tax savings – Contributions, earnings, and qualified healthcare expenses are not subject to federal income tax or state income tax in most states. The maximum HSA contribution for 2021 has increased to $3,600 for single coverage and $7,200 for family. If you are age 55 or older during 2021, you may contribute an additional $1,000.

Interest and investment benefits – You can earn interest each month and have the option to invest in mutual fund families once minimum balance requirements are met. Before selecting your investment options, be sure to consult a fee-only advisor.

Portability – Because you own the HSA, you can take it with you if you change jobs, change health plans or retire.

Rollover – Whatever balance is left in your account at the end of the year, rolls over to the next year. There is no use it or lose it feature.

Age 65 comes with a perk – After reaching age 65, you can also use the money in your HSA for any non-eligible expense, penalty free. However, you will have to pay income taxes on that amount.

Wealth building hack – If you can pay for the expenses (save your receipts) you would usually bill to your HSA account from regular cash flow, this will allow your pre-tax contributions to continue growing at a faster rate. Years down the road, hopefully after your account has grown substantially, you can get reimbursed for the qualifying medical expenses you paid out of pocket.

If you have other medical coverage, you are not eligible to contribute to an HSA (e.g., Medicare or secondary coverage under your spouse’s plan if that plan is not a qualifying HDHP). If you and your spouse are enrolled in an HDHP with an HSA, be sure to monitor your contributions so you do not exceed the family maximum allowable contribution.

Open enrollment is also a good time to determine what your savings goal will be for 2021 and plan accordingly. Additionally, give some thought to securing a revised quote for your homeowners, auto, and liability insurances. You should qualify for an additional discount if you bundle. Instead of the set it and forget it mentality, an annual or bi-annual price check will help determine if you are overspending.

9 Ways to Feel Richer

It is a common belief that financial planners consider the rich as people having $5 million in net worth. However, the numerical classification of rich does not automatically mean someone’s quality of life is rich.

Most people reading this may not ever qualify as being rich from a financial perspective, but that doesn’t mean you can’t feel rich. Here are 9 ways you can begin your journey to feeling rich:

Share new experiences with loved ones – If you’re somewhat adventurous, locate your nearest park and make plans to bathe in nature while exploring a hiking trail. Don’t forget to pack a picnic basket for lunch.

Practice random acts of kindness – Doing something for someone who could not do anything for you in return allows you to practice generosity.

Have more meaningful conversations with friends – Discussions within your circle of influence should not involve more complaints about what’s wrong with the world; instead, try to propose solutions to make things better.

Accomplish a goal – Remember the thing you’ve been saying you’re going to get around to? Do it. Time is a precious commodity so make the most of it.

Revisit moments of joy – Those pictures on your smartphone that you hardly ever look at are a good place to start. If you’re more seasoned in age, track down some old photo albums and reminisce about the old days.

Call an old friend or acquaintance – Remember the last time you heard from someone you hadn’t spoken to in years? That feeling of reconnection probably made your day. Nothing is preventing you from reliving that moment, so call the people you thought of while reading this. (Sending a text message does not count).

Read more – Reading a good book will allow you to go on an emotional journey within the comfort of your own home. If you enjoy sci-fi, mystery, fantasy, or non-fiction, turn to page one and begin.

Engage in arts and crafts – Who cares if you aren’t good at something as long as you feel good doing it? If you like the way painting or learning how to play an instrument makes you feel, do more of it.

Dance like nobody’s watching – Express yourself in any way you see fit. If you’re a little offbeat, who cares? The world would be boring if everyone could do something as well as the next person.

Game Time Budgeting 10 Year Celebration Video Blog

Is Overdraft Protection Worth It?

Overdraft fees collected in 2019 by the 10 largest banks in America was $11 billion dollars. Not shocked yet? You are about to be. The average debit card transaction that triggered an overdraft fee was $20 according to the Center for Responsible Lending. Yes! You read that correctly, twenty dollars.

I have never been a fan of letting someone else count your money, so let’s look at why this activity is so dangerous. First, overdraft protection is a revenue generating product… period. Profits, not you, are being protected. Second, the $35 average overdraft fee is steep considering the bank has immediate access to the money it lends (a very low risk loan) after receiving your next deposit. Third, once you incur one overdraft fee, the likelihood of incurring multiple fees increases based on the number of transactions for which you do not have the money.

A $35 overdraft fee might not sound like much, but that’s because you are not listening. Hmmm! Let’s put this in perspective. Assume you have only a few dollars in your bank account and swipe your debit card for $20. Thanks to overdraft protection, the transaction clears but triggers a $35 fee. Is it me or does this seem similar to a sophisticated form of a payday loan? Don’t let the sexy words fool you.

I know what you are thinking… overdraft protection sounds like something that’s good for you. Who wouldn’t want to be protected from an overdraft? If you think of this as a payday loan, I bet you didn’t realize that the average overdraft loan repayment (remember, you borrowed $20 and paid $35 for the convenience) is only three days. Most payday lenders offer a 14-day repayment plan.

Using the APR (annual percentage rate) calculation from the Payday lending world, let’s shed some light on this math problem. Here’s how it works: Divide the amount of interest paid by the amount borrowed; multiply that number by 365; divide that number by the length of the repayment term; and multiply by 100.

$35/$20 = 1.75 X 365 = 638.75/3 = 212.92 x 100 = 21,291% APR

Please let my math not be correct. Overdraft protection is like payday lending on steroids.

Can you understand why banks love it when customers use overdraft protection? The truly sad part is that 9% of account holders pay 84% of all overdraft fees (approximately $9.24 billion). I understand that banks must earn a return when lending money, but something about this smells a little fishy to me. This is why I am a fan of opting out of overdraft protection. The true protection would come in the form of your card being declined when attempting to make a purchase without having enough money in your account. Protect yourself from yourself and opt out. A declined transaction might be embarrassing in the moment, but that is much better than being broke or minus broke for life.

Credit Tips During a Pandemic

COVID-19 continues to impact all aspects of everyday life. From a financial point of view, I’d bet it has been quite some time since you received a credit card offer. During economic times like this, credit card issuers are focused on controlling risks. When the economy was buzzing along, they had more confidence in people’s ability to make their minimum payment. Nowadays, that confidence has decreased.

Here are a few tips to keep in mind regarding credit:

Be proactive, not reactive: If your household has experienced financial distress during this pandemic, reach out to your creditors immediately and inquire about what type of hardship options are available to you as a consumer. Specifically, regarding credit cards, maybe they will be willing to lower your interest rate, reduce your minimum payment, or waive late fees. You can also try this with your mortgage and auto loan payments.

Reduce your credit utilization ratio: In an effort to control risk, your credit card issuer might decide to lower your credit limit. This action could trigger an increase in your utilization ratio (credit you’re using divided by the amount of credit you have available). If you have a credit card with a limit of $1,000 and you have a $300 balance, your utilization ratio is 30%. If your card issuer suddenly dropped your credit limit to $600, your utilization ratio would then become 50%. The interesting part is that this could also negatively impact your credit score because you are now utilizing more of the credit that is available to you.

Activate Automatic Bill Pay: Most of us like the phrase, “Set it and forget it.” This is how I view auto bill pay, so I never make the mistake of missing a payment. However, I don’t believe in forgetting about any bill that takes money out of your account. This auto draft impacts cash flow and should be tracked accordingly.

Document credit related agreements: When something is not in writing, it never happened. For example, our lawn care company has treated our yard twice this year. Back in March, a customer service representative and I agreed to a one-time lump sum payment for the year. He sent an email which verified our conversation and the price. After making two phone calls, I noticed the one-time payment had not been processed. They continued to bill us for each treatment which would have cost more than the negotiated fee. On June 15, a young lady contacted me about our past due bills (four months after the initial agreement). I explained that our bill was not past due because I had proof of a pre-arranged lump sum payment. She processed the payment and was very apologetic that it had not been taken care of earlier. If I didn’t have proof of the negotiated lower price, it’s possible I would have had to pay the higher per treatment fee.

GTB Celebrates 10 Year Anniversary!

As we celebrate one decade in business, each of our books (click to view books) will be available at a price of only $10 for the next 10 days (sale ends July 10, 2020 at midnight). Thank you for trusting us with your financial wellness needs.

Practical Budgeting Example Post-Layoff Due to COVID-19

In 2010, I was laid off so I thought it might be helpful to create an example of how a household could adjust to a decrease in income. Please note the following:

This example assumes unemployment insurance payments amount to 50% ($1,500/month) of the previous income ($3,000/month). These numbers probably don't reflect your respective income, however, the goal is to understand a concept.

Some budget categories were purposely excluded to save space. However, in a crisis situation, taking care of your necessities is still key.

The percentage of income contributed to each expense category (pre- and post-layoff) is the same except for grocery, student loans, and the credit card payment. For example, because the mortgage is $1,100 and income is $3,000/month, that's 36.67% of net income.

Mortgages that are federally backed qualify for relief which explains the half payment. In reality, you might be able to suspend or reduce payments for up to 12 months.

Federally backed student loans are deferred until Sept. 30, 2020 so $250/month was reallocated to grocery.

$25 for the credit card bill was also reallocated to grocery. Keeping food on the table is crucial.

Some people may receive an additional $600/week ($2,400/month) in unemployment compensation. This is how the total unemployment income could reach $3,900/month. Due to the higher than normal unemployment benefit arrangement because of COVID-19, some people may be earning more while unemployed.